Let me start with a question that's been sitting with me since I finished this book.

Why is finance — arguably the most consequential skill in modern life — the only field where a janitor can consistently outperform a Harvard MBA?

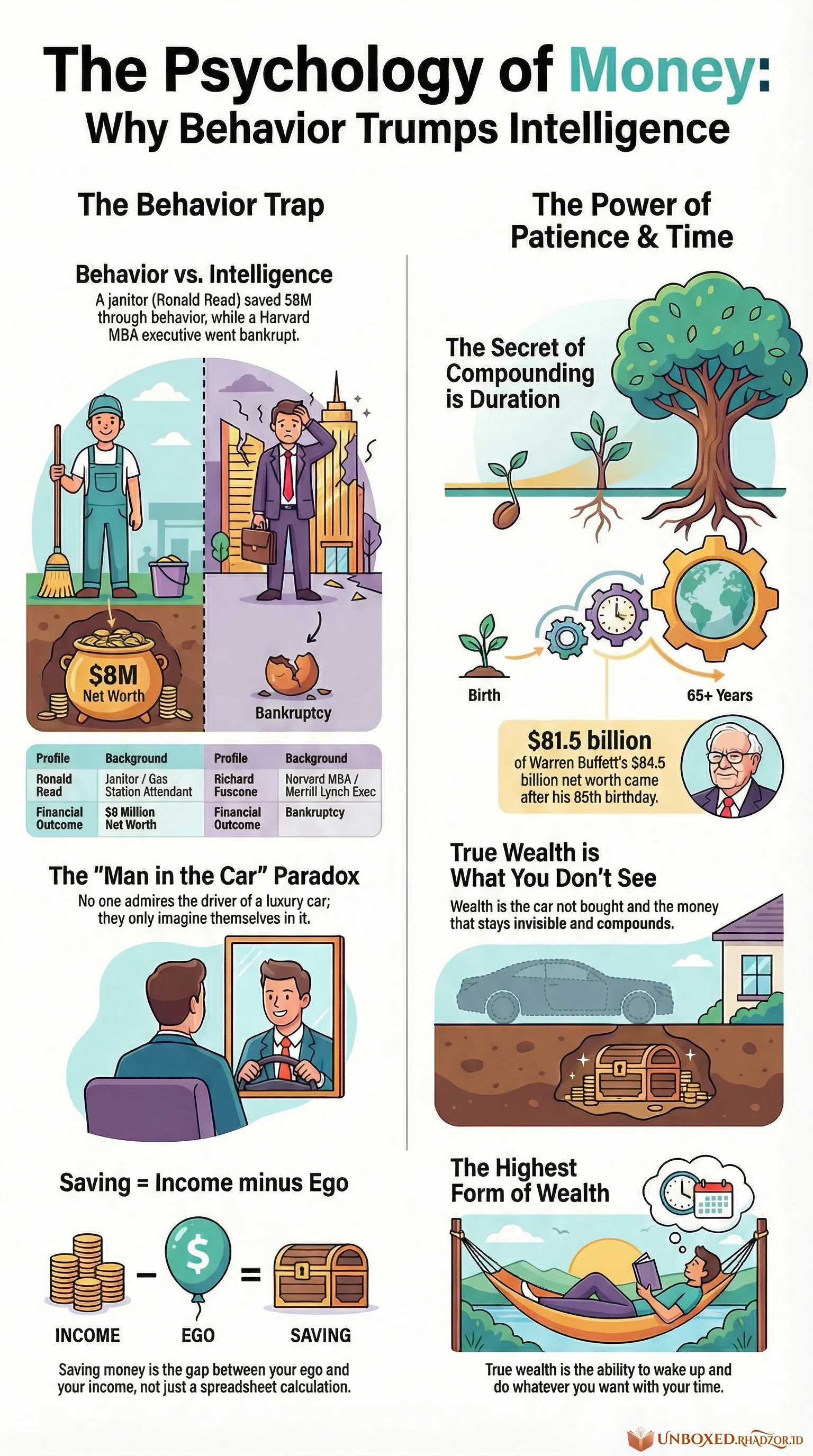

Ronald Read spent his career cleaning floors in Vermont. He died at 92 and left $8 million to a local hospital and library. Around the same time, Richard Fuscone — Merrill Lynch executive, Harvard-educated, the kind of person who gives keynote speeches about wealth management — ended up in bankruptcy court.

Morgan Housel doesn't present this as an inspirational story. He presents it as a structural problem. The game is not won by the most intelligent player. It's won by the player who behaves the best under pressure, over time, without panicking. And that's a completely different skill set than what any MBA program teaches.

---

Here's the thing about money that took me a while to sit with: we've been doing this for, historically speaking, almost no time at all.

The modern financial system — self-directed retirement accounts, consumer debt instruments, mutual funds — is maybe two or three generations old. We've been domesticating dogs for 10,000 years and people still get bitten. Of course we're terrible at managing a 401(k). We're all, functionally, beginners pretending otherwise.

And yet the entire financial media complex — the YouTube channels, the courses, the influencers with whiteboards — operates as if the problem is purely informational. As if you just need to learn the right formula and you'll be fine.

Housel's argument is more uncomfortable than that. The problem isn't what you know. It's how you behave when your portfolio drops 30% and everyone around you is selling.

---

The paradox I keep returning to is one he calls the Man in the Car problem.

Someone buys a Ferrari. The implicit logic is: people will see me in this car and think I'm successful, admirable, someone worth respecting. But Housel points out — with the kind of quiet brutality that good ideas usually have — that nobody looks at the driver. They look at the car and imagine *themselves* in it.

You're not buying admiration. You're financing a fantasy that belongs to someone else.

Sit with that for a second.

Because if that's true, then most status spending is a transaction with no real counterparty. You pay the price. Nobody receives the product. And yet we keep doing it — because the social programming runs deeper than logic, deeper than any book we've read.

*"Wealth is what you don't see."*

Real wealth is the car not bought. The watch not worn. The money that stays invisible, compounding quietly in the background while you live a life that doesn't need to be performed for anyone.

---

The compounding argument is one most people have heard, but I think we've been explaining it wrong.

We frame it as a math problem — here's the formula, here's the graph with the exponential curve. But that framing misses the actual point. Warren Buffett's net worth isn't impressive because of how he invests. It's impressive because of *how long* he's been doing it. $81.5 billion of his $84.5 billion came after he turned 65. The secret isn't the strategy. It's the duration.

Think of it less like a formula and more like a snowball on a very long hill. The size of the snowball at the start barely matters. What matters is whether the hill is long enough — and whether you're still rolling when everyone else has stopped.

The tragedy is that we live in a culture that celebrates acceleration over duration. Everyone wants to be Buffett in a decade. Nobody wants to live like Buffett — boring, patient, consistent, for seventy years.

---

One thing in the book genuinely unsettled me, and I think it should unsettle you too.

Housel observes that pessimism sounds smarter than optimism. The analyst who predicts a crash gets invited on television. The one who says "things will probably be fine" sounds naive, maybe even reckless. We're wired — evolutionarily — to take threats more seriously than opportunities. It kept our ancestors alive on the savannah.

But it distorts how we read the world now.

Historically, markets go up more than they go down. The global economy, for all its chaos, has expanded over time. Optimism, statistically, is the more defensible bet. But it never *sounds* as intelligent as a well-articulated warning. We mistake the feeling of being warned for the feeling of being informed.

That's not wisdom. That's just a cognitive bias dressed in a suit.

---

There's no clean ending to any of this, and I think that's actually the point.

The Psychology of Money doesn't tell you what to buy or when to sell. It doesn't offer a system. What it does — quietly, without making a big deal of it — is hold up a mirror to the gap between how we *think* we make financial decisions and how we actually make them.

And what's in that gap is mostly emotion. History. Ego. The particular economic moment we were born into. The things our parents said or didn't say about money.

*"Saving money is the gap between your ego and your income."*

That line has been stuck in my head for days. Because it reframes the whole conversation. It's not about spreadsheets or strategies. It's about whether you need your choices to be visible to other people in order to feel like they count.

The highest form of wealth, Housel writes, is waking up and being able to do whatever you want that day. Not the yacht. Not the portfolio screenshot. Just time — genuinely yours.

The irony being, of course, that the fastest way to get there is to stop spending money proving you're already there.